Movement in Core Earnings and GAAP earnings were quite different again this quarter and raises red flags about the quality of reported earnings. These results underscore the more stable nature of Core Earnings. Because we remove unusual gains and losses, Core Earnings are not as volatile as GAAP Earnings.

This report is an abridged and free version of S&P 500 & Sectors: GAAP vs Core Earnings Update for 2Q24, one of our quarterly series of reports on fundamental market and sector trends. The full reports are available to Institutional members.

The full version of the report analyzes Core Earnings[1],[2] and GAAP earnings for the S&P 500 and each of its sectors (last analysis is here) from 2004 to present.

This report leverages our cutting-edge Robo-Analyst technology to deliver proven-superior[3] fundamental research and support more cost-effective fulfillment of the fiduciary duty of care.

GAAP Earnings Are Again Misleading in 2Q24

Our superior fundamental data protects investors from being fooled by misleading trends in GAAP Earnings. The recent rise in GAAP Earnings understates the rise in Core Earnings for the S&P 500.

When GAAP earnings and Core Earnings diverged last quarter, we thought we might see the kitchen sink effect accentuate that divergence. So, this quarter’s results are even more interesting. See Figure 1 in the full report.

GAAP Earnings[4] Understate Core Earnings for Over Half of the S&P 500 (by Market Cap)

58% of the companies in the S&P 500 reported GAAP Earnings that are lower than Core Earnings for the TTM ended 2Q24.

When GAAP Earnings understate Core Earnings, they do so by an average of 77%, per Figure 1.

Figure 1: S&P 500 GAAP Earnings Understated by 77% On Average

Sources: New Constructs, LLC and company filings.

We use Funds from Operations (FFO) for Real Estate companies rather than GAAP Earnings.

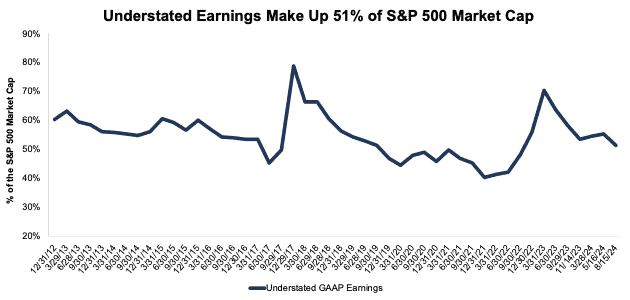

The 288[5] companies with understated GAAP Earnings make up 51% of the market cap of the S&P 500 as of August 15, 2024. Companies with understated GAAP earnings made up 55% of the S&P 500 market cap in as of May 16, 2024 (last quarter’s report).

Figure 2: Understated Earnings as % of Market Cap: 2012 through 8/15/24

Sources: New Constructs, LLC and company filings.

Key Details on Select S&P 500 Sectors

Six of eleven sectors saw a QoQ rise in Core Earnings through the TTM ended 2Q24.

The Technology sector saw the largest QoQ improvement in Core Earnings.

The Technology sector also generates the most Core Earnings. On the flip side, the Real Estate sector has the lowest Core Earnings.

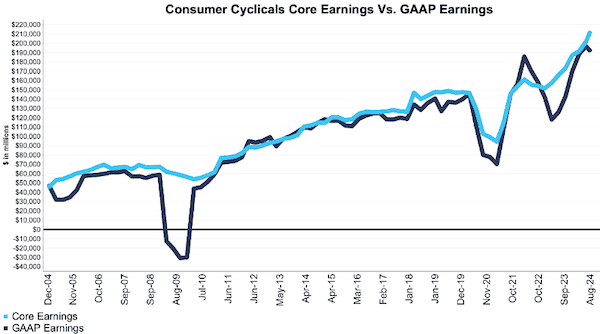

To give you a sense of what we show in the full report, we provide a snippet on the Consumer Cyclicals sector, below.

Sample Sector Analysis[6]: Consumer Cyclicals Sector

Figure 3 shows Core Earnings for the Consumer Cyclicals sector rose 5% QoQ in 2Q24, while GAAP earnings fell 3% over the same time. The full report provides these details and charts on the S&P 500 and all sectors.

Figure 3: Consumer Cyclicals Core Earnings Vs. GAAP: 2004 – 2Q24

Sources: New Constructs, LLC and company filings.

Our Core Earnings analysis is based on aggregated TTM data for the sector constituents in each measurement period.

The August 15, 2024 measurement period incorporates the financial data from calendar 2Q24 10-Qs, as this is the earliest date for which all the calendar 2Q24 10-Qs for the S&P 500 constituents were available

This article was originally published on August 28, 2024.

Disclosure: David Trainer, Kyle Guske II, and Hakan Salt receive no compensation to write about any specific stock, style, or theme.

Questions on this report or others? Join our online community and connect with us directly.

Appendix: Calculation Methodology

We derive the Core Earnings and GAAP Earnings metrics above by summing the Trailing Twelve Month individual S&P 500 constituent values for Core Earnings and GAAP Earnings in each sector for each measurement period. We call this approach the “Aggregate” methodology.

The Aggregate methodology provides a straightforward look at the entire sector, regardless of market cap or index weighting and matches how S&P Global (SPGI) calculates metrics for the S&P 500.

[1] The Journal of Financial Economics features the superiority of our Core Earnings in Core Earnings: New Data & Evidence.

[2] Based on the latest audited financial data, which is the calendar 2Q24 10-Q in most cases. Price data as of 8/15/24.

[3] Our research utilizes our Core Earnings, a more reliable measure of profits, as proven in Core Earnings: New Data & Evidence, written by professors at Harvard Business School (HBS) & MIT Sloan and published in The Journal of Financial Economics.

[4] Overstated companies include all companies with Earnings Distortion >0.1% of GAAP earnings.

[5] For reference, 296 companies reported GAAP Earnings below Core Earnings in the TTM ended 1Q24.

[6] The full version of this report provides analysis for all eleven sectors.