The U.S. Consumer Confidence Index rose again this month to its highest level in more than a year. The more confident people feel spending money, it seems the more investors like to buy stocks. Haha – buying stocks is the easy part. The hard part of investing is figuring out which stocks to buy. And, that is where we come in. We work extremely hard to build financial models that clients can trust to deliver the truth about profitability and valuation. In fact, Ernst & Young published this paper to prove that we are the best at calculating return on invested capital (ROIC).

Why is ROIC important?

It is the one metric statistically shown to be the biggest driver of changes in stock valuations. We like ROIC so much that we made it a key criterion in our Stock Rating methodology.

Then, we went a step further and created a Model Portfolio for companies who tie the compensation of their executives to ROIC. In other words, these companies aim to be sure that executives only get rich if they, first, make shareholders rich. We think that kind of compensation structure is very good.

However, we have to be sure that the company uses a reliable form of ROIC. In other words, there is no point to linking compensation to ROIC if executives are manipulating ROIC to look better than it should. And, trust me, that happens a lot. So, we do the diligence to be sure that a company’s ROIC is reliable before we let it in the Model Portfolio. Fortunately, we’re really good at calculating ROIC; so, we can discern between reliable and unreliable ROICs better than most anyone else.

This Model Portfolio includes stocks that earn an Attractive or Very Attractive rating and align executive compensation with improving ROIC. This combination provides a unique list of long ideas as the primary driver of shareholder value creation is return on invested capital (ROIC).

In our opinion, there’s not a better group of stocks out there as I explain in this special training.

Today’s feature provides a quick summary of how we pick stocks for this Model Portfolio. This summary is not a full Long Idea report, but it gives you insight into the rigor of our research and approach to picking stocks. Whether you’re a subscriber or not, we think it is important that you’re able to see our research on stocks on a regular basis. We’re proud to share our work.

The idea behind featuring stocks and sharing these features with you is to give you free insights into the uniquely high value-add of our research. We want you to know how we do research, so you know more about how reliable research looks and how real Ai and machine learning work.

We’re not giving you the name of the stock featured, because it is only available to our Pro and Institutional members. But, there’s still so much here to share. We want you to see how much work we do and to know where to set the bar when evaluating research providers.

We hope you enjoy this research. Feel free to share with friends and colleagues.

We update this Model Portfolio monthly and November’s Exec Comp Aligned with ROIC Model Portfolio was updated and published for clients on November 15, 2024.

The best performing stock in the portfolio was up 13%. Overall, 7 of the 15 Exec Comp Aligned with ROIC Stocks outperformed the S&P from October 16, 2024 through November 13, 2024.

Stock Feature for November: Energy Company

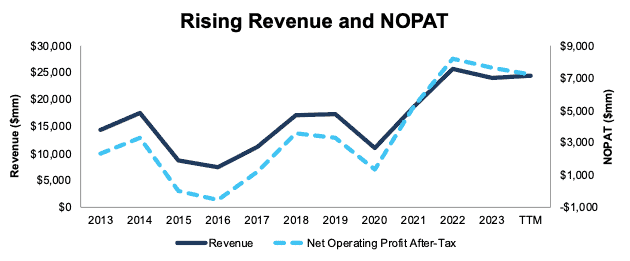

This company has grown revenue and net operating profit after tax (NOPAT) by 5% and 11% compounded annually, respectively, since 2013. The company’s NOPAT margin improved from 19% in 2013 to 30% in the trailing-twelve-months (TTM). Invested capital turns remained the same at 0.5 over the same time but rising NOPAT margins are enough to drive the company’s return on invested capital (ROIC) from 8% in 2013 to 15% in the TTM.

Figure 1: Revenue & NOPAT: 2013 – TTM

Sources: New Constructs, LLC and company filings

Executive Compensation Properly Aligns Incentives

This company’s executive compensation plan aligns the interests of executives and shareholders by adding a modifier based on “Return on Capital Employed” to its annual performance unit awards.

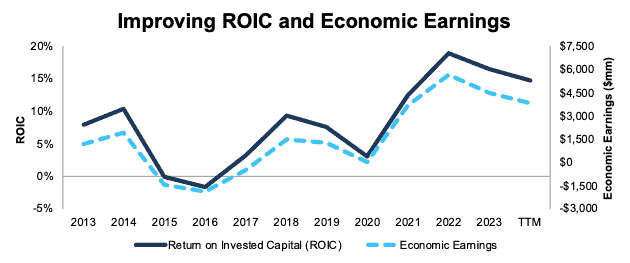

The company’s inclusion of ROCE, a variation of ROIC, as a performance goal has helped create shareholder value by driving higher ROIC and economic earnings. When we calculate ROIC using our superior fundamental data, we find that the company’s ROIC has increased from 8% in 2013 to 15% in the TTM. Economic earnings rose from $1.2 billion to $3.8 billion over the same time.

Figure 2: ROIC & Economic Earnings: 2013 – TTM

Sources: New Constructs, LLC and company filings

This Stock Has Further Upside

At its current price of $132/share, this stock has a price-to-economic book value (PEBV) ratio of 0.8. This ratio means the market expects this company’s NOPAT to permanently fall 20% from current levels. This expectation seems overly pessimistic for a company that has grown NOPAT 13% compounded annually since 2018 and 11% since 2013.

Even if the company’s

- NOPAT margin falls to 23% (below the company’s five-year average margin of 25% and TTM NOPAT margin of 30%) and

- revenue grows 3% (below the 5% in the last ten years) compounded annually through 2033 then,

the stock would be worth $172/share today – a 30% upside. In this scenario, the company’s NOPAT would fall <1% compounded annually from 2023 through 2033.

Should the company grow NOPAT more in line with historical growth rates, the stock has even more upside.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

Below are specifics on the adjustments we made based on Robo-Analyst findings in this featured stock’s 10-Ks and 10-Qs:

Income Statement: we made over $700 million in adjustments with a net effect of removing over $60 million in non-operating expenses. Professional members can see all adjustments made to income statements on the GAAP Reconciliation tab on the Ratings page on our website.

Balance Sheet: we made over $20 billion in adjustments to calculate invested capital with a net increase of over $7 billion. One of the most notable adjustments was several millions in asset write downs. Professional members can see all adjustments made to balance sheets on the GAAP Reconciliation tab on the Ratings page on our website.

Valuation: we made over $16 billion in adjustments with a net decrease of over $5 billion to shareholder value. The most notable adjustment to shareholder value was deferred tax liability. Professional members can see all adjustments to valuations on the GAAP Reconciliation tab on the Ratings page on our website.

…there’s much more in the full report. You can start your membership here or login above to get access to this report and much more.