Winter storm Jonas has hit the East Coast, and it’s predicted to drop so much snow that meteorologists are struggling to come up with adequate adjectives. Meanwhile, investors are doing what they always do, looking for a way to profit. Along with the snows has come the inevitable stream of articles recommending that investors buy the stocks of companies that sell generators, snow blowers, home improvement stores… anything that might experience a bump in demand from the snowstorm.

Beyond the absurdity of basing investment decisions on a temporary weather event, these recommendations can be harmful to investors because they involve some stocks with very shaky fundamentals at a time when market volatility makes investing in strong businesses all the more important.

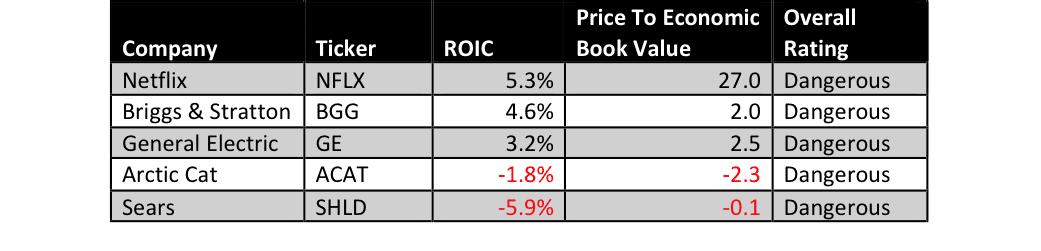

Figure 1: Snow Stocks That Can Bury Your Portfolio

Sources: New Constructs, LLC and company filings.

Figure 1 shows five stocks that have been discussed as “blizzard trades” and also earn our Dangerous rating. They range from companies that sell generators such as General Electric (GE) and Briggs & Stratton (BGG), snowmobile manufacturer Arctic Cat (ACAT), home improvement retailer Sears (SHLD), and even Netflix (NFLX) on the assumption that people stuck inside from the snow will pass the time binge-watching their favorite shows.

These stocks are all dangerous for different reasons. NFLX has an incredibly high price to economic book value (PEBV) of 27. This means that its market valuation is 27 times the perpetuity value of its current cash flows. As we discussed in our analysis of its most recent earnings report, the company’s growth potential does not justify its valuation. Growth in its profitable domestic subscriber base is slowing down, while the company’s international segment looks set to bleed cash for many years to come.

On the other end of the spectrum we have a stock like SHLD that is overvalued at any price. The once-mighty retailer has been losing money for years and shows no sign of turning around. Any slight bump in demand Sears stores might get from the snowstorm will not be nearly enough to reverse its long-term decline, and the company’s only real value at this point is its real estate.

Somewhere in the middle lies BGG. The market expectations aren’t extremely high like they are for NFLX, and the company isn’t burning through cash like SHLD, but a close look at the numbers still reveals a significant gap between the company’s valuation and its true operating cash flow.

Over the past five years, BGG’s net operating profit after tax (NOPAT) has been essentially flat, as has its return on invested capital (ROIC). Despite this stagnation, the current stock price of ~$18/share implies that BGG will grow NOPAT by 7% compounded annually for the next 14 years.

These stocks might get a temporary boost from the winter storm Jonas, but they all have a pronounced disconnect between their profitability and the market’s expectations, and that disconnect is going to catch up to investors sooner or later. Success in the market comes from diligent research, not chasing temporary trends.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, style, or theme.

Click here to download a PDF of this report.

Photo Credit: Ferran Jordà (Flickr)