Two new stocks make our Exec Comp Aligned With ROIC Model Portfolio this month. December’s Exec Comp Aligned With ROIC Model Portfolio was made available to members on 12/15/16.

Recap from November’s Picks

Our Exec Comp Aligned With ROIC Model Portfolio (+8.1%) outperformed the S&P 500 (+3.3%) last month. The best performing stock in the portfolio was Francesca’s Holdings (FRAN), which was up 27%. Overall, 11 out of the 15 Exec Comp Aligned With ROIC Stocks outperformed the S&P in November.

Since inception, this model portfolio is up 23% while the S&P 500 is up 9%.

The success of the Exec Comp Aligned With ROIC Model Portfolio highlights the value of our forensic accounting (featured in Barron’s). Return on invested capital (ROIC) is the primary driver of shareholder value creation. By analyzing footnotes in SEC filings, we are able to calculate an accurate and comparable ROIC for 3000+ companies under coverage.

This Model Portfolio only includes stocks that earn an Attractive or Very Attractive rating and align executive compensation with improving ROIC. We think this combination provides a uniquely well-screened list of long ideas.

New Stock Feature for December: AutoZone Inc. (AZO: $789/share)

AutoZone (AZO), automotive parts retailer, is one of the additions to our Exec Comp Aligned With ROIC Model Portfolio in December. We first featured AutoZone in February 2014 when we highlighted its exceptional corporate governance and decision to use ROIC to, as AutoZone puts it, “evaluate whether we are effectively using our capital resources”. AZO is up 46% since this initial report, yet remains undervalued.

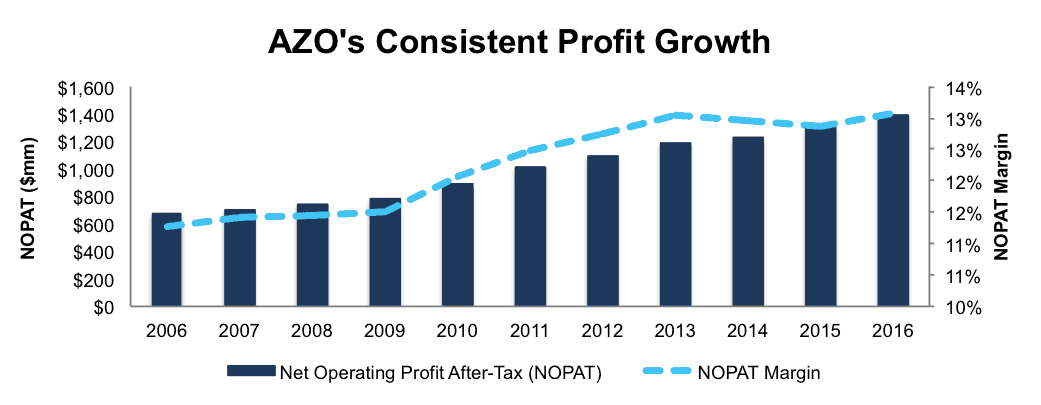

Over the past decade, AutoZone has grown revenue 6% compounded annually, and, more importantly, after-tax profit (NOPAT) by 8% compounded annually. Over the same time, AutoZone has improved its NOPAT margin from 11% in 2006 to 13% in 2016, per Figure 1.

Figure 1: AutoZone’s Decade of Profit Growth

Sources: New Constructs, LLC and company filings

The company currently earns a top-quintile ROIC of 24% and has generated cumulative $4.5 billion in free cash flow over the past five years.

Executive Compensation Aligned With ROIC Creates Shareholder Value

AutoZone added return on invested capital to its executive compensation plan in 2002, and, as noted above, management uses ROIC “to evaluate whether we are effectively using our capital resources and believe it is an important indicator of our overall operating performance.” We’ve detailed ways in which ROIC is directly correlated to changes in shareholder value here, and AZO’s use of ROIC to measure performance ensures executives’ interests are aligned with shareholders’ interests.

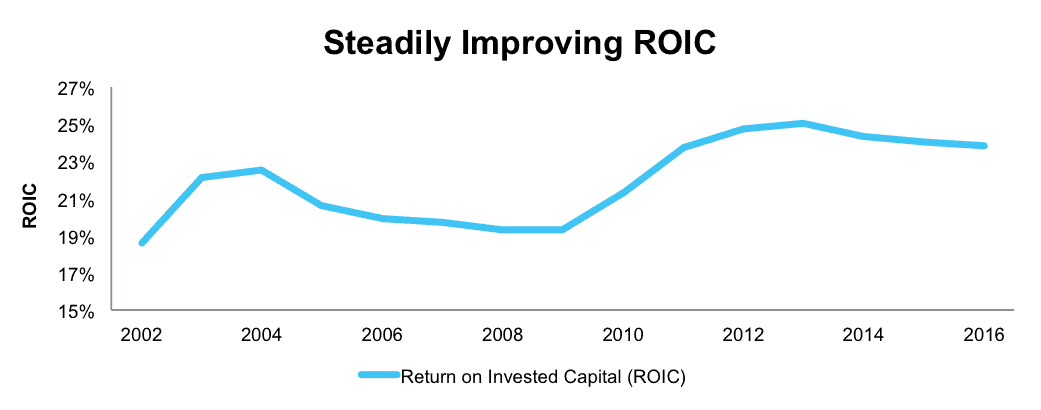

AZO’s ROIC has improved from an already impressive 18% in 2002 to 24% in 2016. Even during the 2008/2009 economic recession, which greatly impacted the auto industry, AutoZone still earned a 19% ROIC, as seen in Figure 2.

Figure 2: ROIC Improvement Since Adding to Executive Compensation Plan

Sources: New Constructs, LLC and company filings

In 2016, ROIC, along with EBIT, were the two metrics used to determine annual cash incentive awards. These annual incentives make up 10% of the CEO’s compensation plan and 17% of other executives’ pay. Investors should see less risk and more upside in stocks where management incentivizes focus on ROIC and avoids questionable non-GAAP metrics.

AZO Remains Undervalued

Despite AutoZone’s share price increasing 46% since our initial report, and 7% year-to-date, shares remain significantly undervalued. At its current price of $789/share, AZO has a price-to-economic book value (PEBV) ratio of 1.2. This ratio means the market expects AZO’s NOPAT to grow by only 20% over the remainder of its corporate life. This expectation seems rather pessimistic for a firm that has grown NOPAT by 8% per year over the past decade.

If AutoZone can maintain 13% NOPAT margins (five year average) and grow NOPAT by 5% compounded annually for the next decade, the stock is worth $995/share today – a 26% upside.

Impacts of Footnotes Adjustments and Forensic Accounting

In order to derive the true recurring cash flows, an accurate invested capital, and a real shareholder value, we made the following adjustments to AutoZone’s 2016 10-K:

Income Statement: we made $366 million of adjustments with a net effect of removing $148 million in non-operating expense (1% of revenue). We removed $257 million related to non-operating expenses and $109 million related to non-operating income. See all adjustments made to AZO’s income statement here.

Balance Sheet: we made $2.4 billion of adjustments to calculate invested capital with a net increase of $1.9 billion. The most notable adjustment was $1.7 billion (42% of reported net assets) related to operating leases. See all adjustments to AZO’s balance sheet here.

Valuation: we made $7.6 billion of adjustments with a net effect of decreasing shareholder value by $7.6 billion. There were no adjustments that increased shareholder value. Apart from the $1.6 billion in off-balance sheet debt, the most notable adjustment to shareholder value was the removal of $436 million due to outstanding employee stock options. This adjustment represents 2% of AutoZone’s market value. Despite the net decrease in shareholder value, AZO remains undervalued.

This article originally published here on December 16, 2016.

Disclosure: David Trainer, Kyle Guske II, and Kyle Martone receive no compensation to write about any specific stock, style, or theme.

Scottrade clients get a Free Gold Membership ($588/yr value) as well as 50% discounts and up to 20 free trades ($140 value) for signing up to Platinum, Pro or Unlimited memberships. Login or open your Scottrade account & find us under Quotes & Research/Investor Tools.

Click here to download a PDF of this report.

Photo Credit: taxcredits.net (Flickr)