We published an update on this Long Idea on May 19, 2021. A copy of the associated Earnings Update report is here.

Warren Buffet’s advice to “be fearful when others are greedy, and be greedy when others are fearful,” presents an interesting conundrum for investors considering The Walt Disney Company (DIS: $109/share). Over the past two years, the market has displayed equal parts greed (when it comes to Disney’s booming movie business) and fear (over cord-cutters putting pressure on ESPN’s business model).

Buffet’s advice could arguably be applied in either direction. We believe the fears over ESPN are overblown and represent a short-term challenge, while the strength of Disney’s movie franchises should have a positive impact on numerous other business segments to continue the long-term growth of the business.

Impressive Track Record Of Success

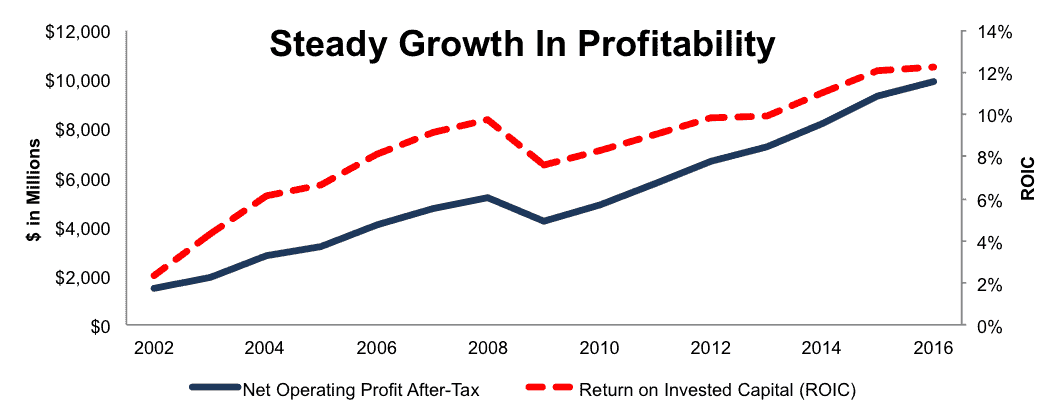

Few companies can match Disney’s consistent growth in profitability over the past decade and a half. Since 2002, Disney has grown after-tax profit (NOPAT) by 15% compounded annually while improving its return on invested capital (ROIC) from 2% to 12%. As Figure 1 shows, both metrics have trended up in every year except for 2009 over that time.

Figure 1: Disney’s Profitability Since 2002

Sources: New Constructs, LLC and company filings.

Disney’s current 12.3% ROIC is higher than any of the other large media conglomerates, including Fox (FOXA), Comcast (CMCSA), Viacom (VIAB), and Time Warner (TWX). In addition, it’s the only one of these companies to have positive and rising economic earnings.

True Platform Value

Over the past couple years, we’ve often pushed back against companies that grow aggressively through acquisitions. Most notably, we criticized Bill Ackman’s claim that the “platform value” of companies like Valeant (VRX) justified lofty valuations and overpriced acquisitions.

While our skepticism of Valeant has been validated, that doesn’t mean we reject the concept of platform value. Some companies really do have a platform that allows them to acquire competitors and unlock hidden value. Disney is one of those companies.

No other company can match Disney in terms of brand value, creative expertise, or the breadth of its content monetization channels. These assets enable the company to buy up beloved intellectual property (Pixar, Marvel, LucasFilm), churn out blockbusters, and then aggressively monetize the success of those films through theme park attractions, licensed toys, and spin-off TV series.

Investors miss the point when they point to the relatively small (17% of operating income) size of the film division. The true magic of Disney is that it continues to rake in cash from its films years after they leave the box office.[1] By monetizing IP better than anyone else, Disney has a unique ability to grow through acquisitions in a way that creates real value for shareholders, as evidenced by its rising ROIC.

ESPN Concerns Are Overstated

Every time Disney has another hit, you can count on the bears to come out of their dens and grumble about how ESPN subscriber numbers, not box office receipts, are what really matter.

It is true that ESPN has been shedding subscribers recently, although there’s some debate as to exactly how many it’s losing. What you don’t often hear in these debates is that this subscriber loss didn’t start in the past couple of years. ESPN’s subscriber numbers actually peaked in 2010 at 100 million. They’ve since dropped to 90 million. As you’ll remember from Figure 1, that hasn’t stopped Disney from doubling its NOPAT (and tripling its stock price).

The drop in subscribers comes from cord-cutters, many of whom were not watching ESPN in the first place. Core demand for ESPN hasn’t changed, which is why the network has been able to keep raising its affiliate fees to compensate for declining subscriber numbers.

Many analysts treat cord-cutting as an existential threat to the business model of TV networks, but it’s really just a change to the means of distribution. There may be some short-term disruption to ESPN’s profits as it learns the best way to deliver its content through live streaming services, but the long-term outlook is strong. Live sports rights remain some of the most valuable commodities in the media business.

Fears Lead To Cheap Valuation

Let’s take a moment to consider Disney’s accomplishments over the past year and a half. Since the summer of 2015, Disney has:

- Successfully restarted the Star Wars franchise with Force Awakens

- Proved it can expand the Star Wars universe with Rogue One, opening up the potential for scores of new movies and licensable characters, content, and merchandise

- Had several other $1 billion+ movies with Zootopia, Finding Dory, and Captain America: Civil War

- Grown NOPAT by 14% in 2015 and 6% in 2016

- Increased its ROIC from 11% to 12.3%

- Expanded its reach in China with the opening of Shanghai Disney

One might reasonably expect the market to reward a company with those achievements. Instead, DIS is down 7% since July 1, 2015. This disconnect creates a compelling value opportunity in the stock.

At its current price of $109/share, Disney has a price to economic book value ratio of just 1.2, which implies that the market expects that the company will grow NOPAT by no more than 20% over the remainder of its corporate life.

If Disney can grow NOPAT by just 4% compounded annually over the next 15 years, the stock has a fair value of $137/share today, which is a 26% upside from the current stock price. The company has grown NOPAT by 15% compounded annually over the past 15 years, so 4% annual growth seems like a conservative estimate.

Potential catalysts for the stock price to break out of its rut include:

- New value creating acquisitions

- A successful standalone streaming service from ESPN (or a spinoff at the right valuation)

- Further expansion in China

- More blockbusters, whether that’s the Star Wars and Marvel universes exceeding expectations, success from the live action Beauty and the Beast, or the relaunch of the Indiana Jones franchise in 2019.

Buyback Plus Dividend Yield of 5.7%

In 2016, Disney repurchased $7.5 billion worth of stock (4.3% of its market cap). The company has over $30 billion remaining on its buyback authorization, so there’s no reason to expect a slowdown in the pace of buyback activity. In fact, with the completion of Shanghai Disney, we may see even greater free cash flow from Disney going forward, which would support even more capital return.

Combine Disney’s buyback with its 1.4% dividend yield, and the company returns roughly 5.7% of its market cap to shareholders annually.

Executive Compensation Leads To Responsible Management

Roughly 90% of compensation for Disney executives comes in the form of performance-based bonuses. 25% of performance-based compensation is tied to ROIC. Even better, Disney calculates ROIC in a fairly rigorous manner (better than most) that lines up well with economic reality.

ROIC is the primary driver of shareholder value, so we appreciate Disney tying a significant portion of executive’s bonuses to this important metric. Holding executives accountable for efficient capital allocation decisions can help companies outperform their industry peers, as demonstrated by the performance of our Executive Compensation Tied to ROIC portfolio (23% vs. 9% for the S&P 500 since inception).

Disney’s compensation practices give us confidence that management will continue to be responsible stewards of shareholder capital. Rumors continue to swirl that Disney might buy Netflix (NFLX) or Twitter (TWTR), but either of these acquisitions would have a large negative impact on ROIC. Disney’s executive compensation incentives penalize management for such value-destroying acquisitions.

Impact of Footnotes Adjustments and Forensic Accounting

In order to derive the true recurring cash flows, an accurate invested capital, and an accurate shareholder value, we made the following adjustments to Disney’s 2016 10-K:

- Income Statement: We made $1.4 billion of adjustments, with a net impact of removing $498 million of non-operating expense. We removed the impact of a $129 million write-down due to the discontinuation of the Infinity Console business. You can see all the adjustments made to DIS’s income statement here.

- Balance Sheet: We made $11.4 billion of adjustments, with a net impact of adding $5.2 billion to invested capital. The largest adjustment was adding $4 billion back due to accumulated other comprehensive income. You can see all the adjustments made to DIS’s balance sheet here.

- Valuation: We made $40.9 billion of adjustments with a net impact of decreasing shareholder value by $33.5 billion. The largest adjustment was the removal of $23.5 billion due to total debt, including $2.4 billion to off-balance sheet debt. You can see all the adjustments made to DIS’s valuation here.

Minimal Insider Selling And Short Interest

Over the past 12 months, Disney insiders have bought 25 thousand shares and sold 438 thousand shares for a net effect of 413 thousand shares sold, or less than a tenth of a percent of Disney’s total shares outstanding. Short interest is also relatively low at just under 2 percent. ESPN’s struggles have attracted some negative attention, but the strength of the rest of the business, along with a cheap valuation, seem to be scaring shorts away.

Attractive Funds That Hold DIS

The following funds receive our Attractive-or-better rating and allocate significantly to Disney.

- iShares US Consumer Services ETF (IYC): 4.8% allocation and Attractive rating

- SPDR Dow Jones Industrial Average ETF Trust (DIA): 3.6% allocation and Very Attractive rating

- American Century Mutual Funds: Select Fund (ASERX): 3.1% allocation and Very Attractive rating

- Valued Advisors Trust: BFS Equity Fund (BFSAX): 3% allocation and Attractive rating

This article originally published here on January 11, 2016.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, style, or theme.

[1] Example: My two year-old niece received a Frozen dress, cape, jacket, and book for Christmas this year.

Click here to download a PDF of this report.

Scottrade clients get a Free Gold Membership ($588/yr value) as well as 50% discounts and up to 20 free trades ($140 value) for signing up to Platinum, Pro, or Unlimited memberships. Login or open your Scottrade account & find us under Quotes & Research/Investor Tools.

Photo Credit: Free Press (Flickr)