Long Idea and Danger Zone research reports are part of our efforts to identify hidden gems in the market and also help clients avoid portfolio blowups. Position Update reports serve as notification that one or more key factors underlying our original report have changed.

Spirit AeroSystems (SPR: $78/share) – Maintaining Long Position – SPR +40% vs. S&P +3%

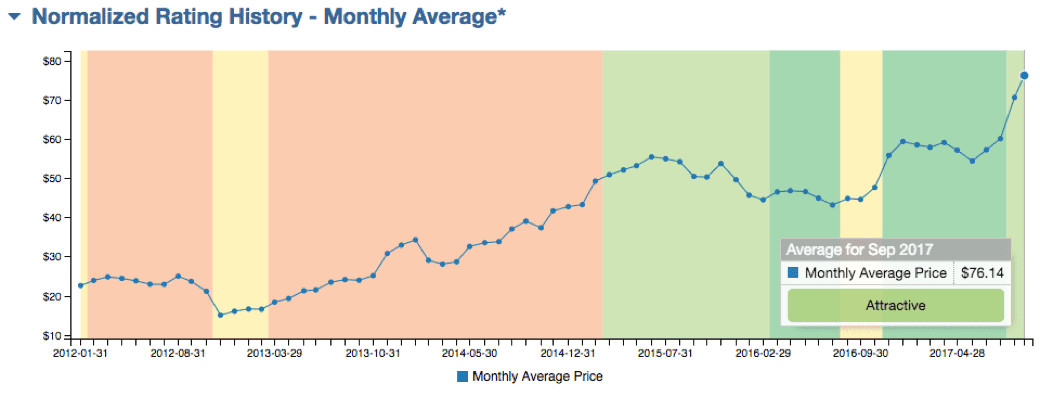

Spirit AeroSystems (SPR) was selected as a Long Idea on 6/26/17 in An Undervalued Stock That’s Ready for Take-Off. SPR earned a Very Attractive risk/reward rating at the time due to its high return on invested capital (ROIC), high free cash flow (FCF) yield, and low price-to-economic book value (PEBV) ratio.

Following a 27% gain driven by strong 2Q17 earnings and a new Boeing contract, SPR’s risk/reward rating was downgraded one level to Attractive on 8/7/17 due to higher market-implied expectations. The shares have risen an additional 13% since, but still earn an Attractive rating as of 9/22/17. Current fundamental and valuation highlights underlying SPR’s Attractive rating include:

- Economic EPS is 84% of GAAP EPS for SPR vs. 41% for Industrials and 36% for the S&P 500.

- ROIC of 14% for SPR ranks in second quintile overall vs. 9% for Industrials.

- FCF Yield of 10% for SPR vs. 1% for Industrials and 2% for the S&P 500.

- PEBV valuation of 1.3 for SPR vs. 2.2 for Industrials and 2.5 for the S&P 500.

- Growth Appreciation Period (GAP) of <1 year vs. 27 years for Industrials and 23 for S&P 500.

SPR continues to offer an attractive risk/reward trade-off based on potential upside to low market-implied expectations for future profit growth. To justify the current price of $78/share, SPR must grow NOPAT by just 1% compounded annually over the next ten years. If SPR can grow NOPAT by 3% compounded annually over the next ten years, the stock is worth $95/share today – a 21% upside. This scenario assumes a stable NOPAT margin of 8% and revenue growth of 4% compounded annually.

Figure 1: SPR Stock Price and Risk/Reward Rating History

Sources: New Constructs, LLC and company filings

This article originally published on September 22, 2017.

Disclosure: David Trainer, Kyle Guske II, and Kenneth James receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.