Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

Beginning in 4Q17, we separated the Real Estate sector from the Financials sector in order to provide better insights into these two very different market segments. Based on our 4Q17 Sector Ratings for ETFs and Mutual Funds, the Real Estate sector ranks 10 out of 11 and receives an Unattractive rating. As a whole, the Real Estate sector is filled with potential pitfalls. Only 3% of Real Estate ETFs and mutual funds receive an Attractive-or-better rating while 82% receive an Unattractive-or-worse rating.

A deeper level of diligence remains warranted, however, and reveals that some of these funds are worse than others. Digging further, we identified a potentially dangerous fund that traditional, backward-looking fund research overlooks. We found this fund by leveraging our Robo-Analyst technology to sift through the holdings of all 206 Real Estate ETFs and mutual funds.[1] We think a holdings-level analysis is important to fulfilling the Fiduciary Duty of Care.

Neuberger Berman Real Estate Fund (NREAX, NRECX, NRERX, NBRFX, NBRIX, NRREX) is one of the Real Estate funds investors should avoid. All six classes earn a Very Unattractive rating and NREAX is the worst of the group. The fund’s poor holdings and high fees diminish the likelihood that the fund’s will outperform moving forward. Neuberger Berman Real Estate Fund is in the Danger Zone this week.

Holdings Quality Analysis Reveals Poor Allocation vs. Benchmark

The only justification for a mutual fund to charge higher fees than its passively-managed ETF benchmark is “active” management that leads to out-performance. A fund is most likely to outperform if it has higher quality holdings than its benchmark. To make this determination on holdings quality, we leverage our Robo-Analyst technology to drill down to the individual stock level of every fund.

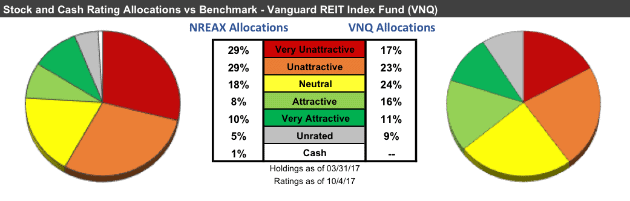

Figure 1: Neuberger Berman Real Estate Fund (NREAX) Asset Allocation

Sources: New Constructs, LLC and company filings

Per Figure 1, Neuberger Berman Real Estate Fund allocates only 18% of its assets to Attractive-or-better rated stocks compared to 27% for the Vanguard REIT Index Fund (VNQ). In addition, exposure to Unattractive-or-worse rated stocks is much higher for Neuberger Berman Real Estate Fund (58% of assets) than for VNQ (40% of assets).

Furthermore, seven of the mutual fund’s top 10 holdings receive a Dangerous-or-worse rating and make up 31% of its portfolio.

Given the unfavorable distribution of Attractive vs. Unattractive allocations relative to the benchmark, Neuberger Berman Real Estate Fund appears poorly positioned to capture upside potential while minimizing downside risk.

Neuberger Berman Allocates to Overvalued Real Estate Stocks

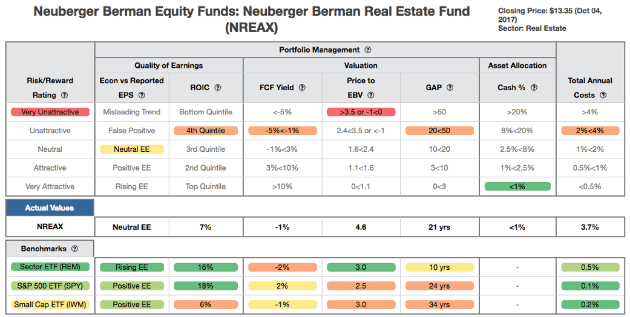

In Figure 2, the details behind our Predictive Overall Fund rating for NREAX show the managers of the fund have selected highly overvalued stocks when compared against the benchmark. These criteria we use to rate funds are very similar to our Stock Rating Methodology, because the performance of a fund’s holdings equals the performance of a fund.

Figure 2: Neuberger Berman Real Estate Fund (NREAX) Rating Breakdown

Sources: New Constructs, LLC and company filings

The return on invested capital (ROIC) for NREAX’s holdings is 7%, which is well below the 18% for S&P 500 companies. The -1% free cash flow (FCF) yield of NREAX’s holdings is and lower than VNQ (1%) and the S&P 500 (2%).

The price to economic book value (PEBV) ratio for the S&P 500 and VNQ is 2.5 and 4.0 respectively. Meanwhile, the PEBV ratio for NREAX is 4.6. This ratio means the market expects NREAX profits to grow at nearly double the rate of companies in the S&P 500 and 60% greater than those held by the benchmark.

Lastly, our discounted cash flow analysis of fund holdings reveals a market implied growth appreciation period (GAP) of 21 years for NREAX compared to just 14 years for VNQ. In other words, companies held by NREAX have to grow economic earnings for seven years longer than those in the benchmark to justify their current stock prices. This expectation seems even more unlikely given that NREAX holds less profitable firms as measured by ROIC.

Ultimately, the high profit growth expectations baked into the valuations of stocks held by NREAX lowers the upside potential and makes outperformance less likely.

Neuberger Berman Real Estate Fund’s Fees Make Outperformance More Difficult

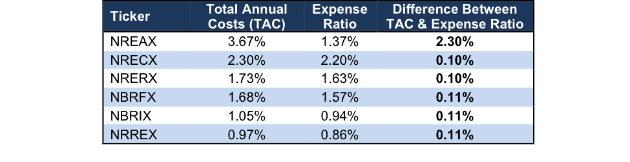

At 3.67%, NREAX’s total annual costs (TAC) are higher than 91% of Real Estate sector mutual funds under coverage. For comparison, the average TAC of all Real Estate sector mutual funds under coverage is 1.94%, the weighted average is 0.92%, and the benchmark ETF (VNQ) has total annual costs of 0.13%. Per Figure 3, Neuberger Berman Real Estate Fund’s expense ratios understate the true costs of investing in this fund. Our TAC metric accounts for more than just expense ratios. We take into account the impact of front-end loads, back-end loads, redemption fees and transaction costs. Transaction costs add 11 basis points to the TAC based on annual portfolio turnover of 49%.

Figure 3: Neuberger Berman Real Estate Fund’s Cost Comparison

Sources: New Constructs, LLC and company filings

To justify its higher fees, this fund must outperform its benchmark by the following over three years:

- NREAX must outperform by an average of 3.54% annually.

- NRECX must outperform by an average of 2.17% annually.

- NRERX must outperform by an average of 1.60% annually.

- NBRFX must outperform by an average of 1.55% annually.

- NBRIX must outperform by an average of 0.92% annually.

- NRREX must outperform by an average of 0.84% annually.

An in-depth analysis of NREAX’s TAC is on page 2 here.

Underperformance Looks Likely to Continue

Year-to-date, NREAX is up 6% while VNQ is up 1%. Given that 58% of assets are allocated to stocks with Unattractive-or-worse ratings, the recent price outperformance looks unlikely to continue.

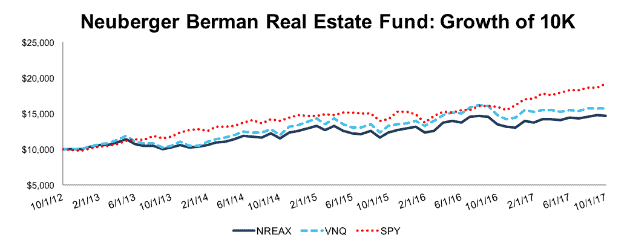

Investors looking to buy NREAX must not only expect the significant profit growth highlighted earlier, but also ignore the fund’s failure to outperform over the past five years. Figure 4 shows the growth of 10k for NREAX, VNQ, and SPY

We think it overly optimistic to invest in the belief that this mutual fund will outperform its much cheaper ETF benchmark over significant time frames given the issues outlined above.

Figure 4: Neuberger Berman Real Estate Fund vs. VNQ & SPY

Sources: New Constructs, LLC and company filings.

The Importance of Holdings Based Fund Analysis

Our ETF & mutual fund ratings provide forward looking diligence by analyzing the risk/reward of the holdings of every fund. This unique approach to mutual fund analysis shows that investors must be careful when investing in funds. Rather than putting money into NREAX, investors would be better suited with one of the Real Estate funds that receive an Attractive-or-better rating.

Each quarter we rank the 11 sectors in our Sector Ratings for ETF & Mutual Funds and the 12 investment styles in our Style Ratings For ETFs & Mutual Funds report. This analysis allows us to find funds that investors using traditional fund research may view as quality investments while deeper analysis reveals otherwise, such as Neuberger Berman Real Estate Fund.

This article originally published on October 9, 2017.

Disclosure: David Trainer, Kyle Guske II, and Kenneth James receive no compensation to write about any specific stock, sector, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Ernst & Young’s recent white paper “Getting ROIC Right” proves the superiority of our holdings research and analytics.

Click here to download a PDF of this report.

Photo Credit: Jan Hedström (Flickr)