We closed this position on August 18, 2021. A copy of the associated Position Update report is here.

The Financials Sector is currently our top-rated sector and earns our Very Attractive rating. Financials have underperformed significantly over the past five years, which means that valuations are well-below the overall market. Investors seeking value have lots of options in this sector. Growth, on the other hand, is harder to find. Aggregate economic earnings for the sector have been flat for the past four years.

This regional bank has bucked the trend in the rest of the sector by delivering solid growth in recent years, even as its valuation remains cheap. Lakeland Financial Corp (LKFN: $48/share) is this week’s Long Idea.

Long-Term Track Record of Growth

Lakeland Financial is a holding corporation that owns and operates Lake City Bank, a small regional bank with 50 branches throughout north and central Indiana. Over the years, LKFN has expanded from the small town of Warsaw in northern Indiana to cover large portions of the region. In 2011, the company opened its first branch in Indianapolis.

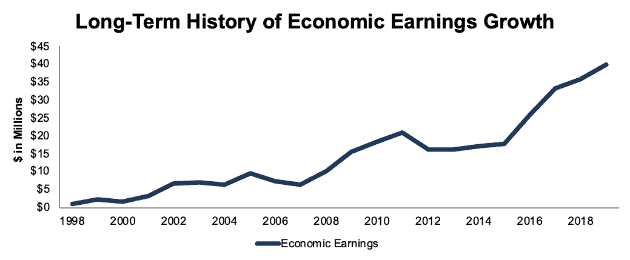

What stands out about LKFN’s growth is its consistency. The company has grown economic earnings in 15 out of the past 20 years, per Figure 1. Only once, in 2006 and 2007, have economic earnings declined in consecutive years.

Figure 1: LKFN’s Economic Earnings Since 1998

Sources: New Constructs, LLC and company filings

Figure 1 also shows that economic earnings growth has accelerated in recent years. From 2015-2018, economic earnings grew by 26% compounded annually. Over the trailing twelve months (TTM) period, economic earnings are up 9% year-over-year.

In addition, LKFN boasts a highly consistent return on invested capital (ROIC). Dating back to 1998, the company has earned an ROIC of 10% or higher in every year except 2015, when its ROIC was 9.9%.

Cost Control Drives Competitive Advantage

As the company highlights in its investor presentations, management is focused on “blocking and tackling”. Solid execution and cost control drive consistent profit growth. LKFN aims to maximize efficiency and find long-term organic growth rather than make splashy acquisitions.

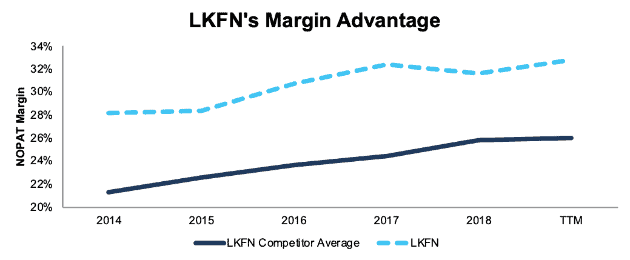

This strategy has paid off. LKFN’s efficiency ratio – non-interest expense divided by total net revenue – is just 45%. For comparison, LKFNs peers have an average efficiency ratio in the mid-50’s. In other words, it costs LKFN less to generate $1 in revenue than its peers.

Our own data backs up this conclusion. Over the past five years, LKFN has consistently maintained a margin ~7 percentage points higher than the peers listed in its proxy statement, per Figure 2.

Figure 2: LKFN NOPAT Margin vs. Peers: 2014-TTM

Sources: New Constructs, LLC and company filings

Focus on Training and Company Culture

LKFN’s emphasis on employee training and strong company culture help drive it superior efficiency. The company uses its corporate university – Lake City University – to provide training and instruction for all its employees.

One of the reasons LKFN doesn’t engage in acquisitions is that company doesn’t want to dilute its strong culture.

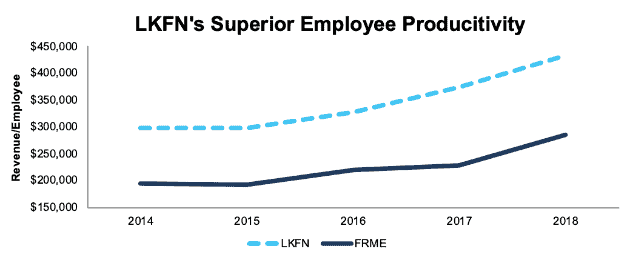

The success of LKFN’s strategy shows up in the superior revenue/employee that it generates compared to its closest competitor, First Merchants Corp (FRME). In 2018, LKFN earned $239 million in revenue with 553 full-time employees, or $432 thousand for each employee. FRME, on the other hand, earned $484 million in revenue with 1,702 employees, or $285 thousand for each employee.

Figure 3: LKFN vs. FRME: Revenue/Employee 2014-2018

Sources: New Constructs, LLC and company filings

Figure 3 shows that over that past five years, LKFN has consistently earned ~50% more revenue/employee than FRME. Since employee compensation accounted for 56% of LKFN’s non-interest expense in 2018, maximizing employee productivity is crucially important to growing profits.

Competitive Threat of Big Banks is Overblown

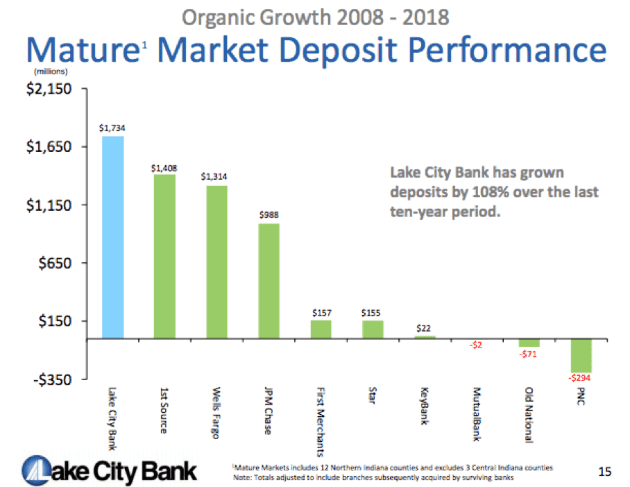

LKFN doesn’t just compete against other regional banks, it also faces significant pressure from national banks such as JP Morgan Chase (JPM) and Wells Fargo (WFC). Bears might worry that these mega-banks, with their superior scale and resources, would be able to undercut LKFN and put it out of business. However, Figure 4 shows that LKFN has grown its deposits faster than these big banks in its core market.

Figure 4: LKFN Deposit Growth vs. Competitors

Sources: LKFN Investor Relations

LKFN’s growth runs counter to the popular narrative that technology has killed the bank branch and made it impossible for smaller banks to compete. In fact, a recent survey found that even Millennials still rank “Convenient Branches” as their number one priority when choosing a bank.

With big banks closing branches across the country, smaller banks like LKFN have seized the opportunity to win new customers and expand their footprint. These banks provide a personalized service and connection to the community that big banks can’t replicate.

In addition, LKFN has invested in technology to keep its services competitive by:

- Improving cybersecurity

- Increasing adoption of its mobile app

- Decreasing administrative costs

- Leveraging data gathering and analysis to provide superior advice to clients and identify cross-selling opportunities

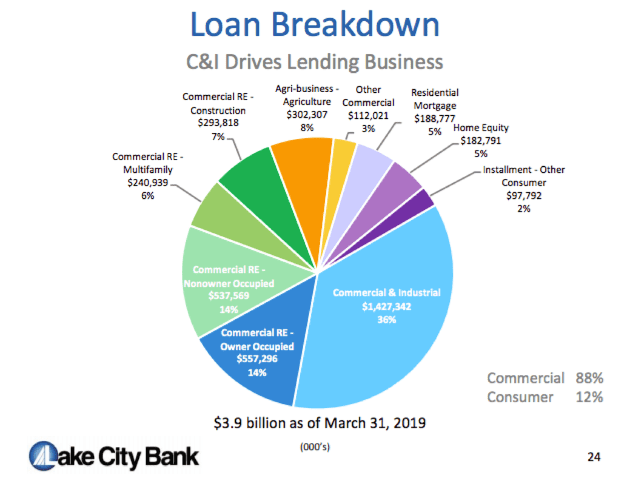

Diversified Loan Base Reduces Risk

LKFN has a well-diversified loan portfolio with exposure to commercial and industrial, real estate, agriculture, and residential lending. The bank’s significant diversification means there’s little risk of an industry-specific shock (i.e. a housing market crash) sinking its entire business.

Figure 5: LKFN’s Loan Portfolio Breakdown

Sources: LKFN Investor Relations

In addition to being well diversified, LKFN’s loan portfolio appears to be high quality. Nonperforming loans totaled just $6.6 million in Q1 2019, or less than 0.2% of all loans. Meanwhile, LKFN’s loan loss reserve is $49.6 million, or ~1.3% of all loans. The company’s strong reserve position should further cushion it in the event of a downturn.

New Income Sources Can Compensate for Interest Rate Risk

One of the biggest risks investors face with LKFN is the threat that falling interest rates could hurt its net interest income. LKFN projects that a 0.25% decrease in interest rates would lead to a 2% decline in net interest income, while a 1% decrease in rates would lead to an 8% decline. The company’s net interest income of $145 million in 2018 was more than three times higher than its non-interest income of $40 million, so any decline in interest rates would be significant to LKFN results.

However, LKFN has other sources of revenue that could offset part of the decline in the event of a rate decrease. The company’s revenue from wealth advisory fees has increased by 15% compounded annually over the past two years, from $4.8 million in 2016 to $6.3 million in 2018.

The company has significantly increased the share of its deposits from commercial accounts in recent years, too. Since these accounts pay significantly higher fees, this growth has contributed to the company’s non-interest income. Service charges on deposit accounts have also increased by 15% compounded annually over the past two years, from $12 million in 2016 to $15.8 million in 2018.

These new revenue sources don’t eliminate the interest rate risk for LKFN, but do provide a potential source of growth that can make an interest rate decrease less painful.

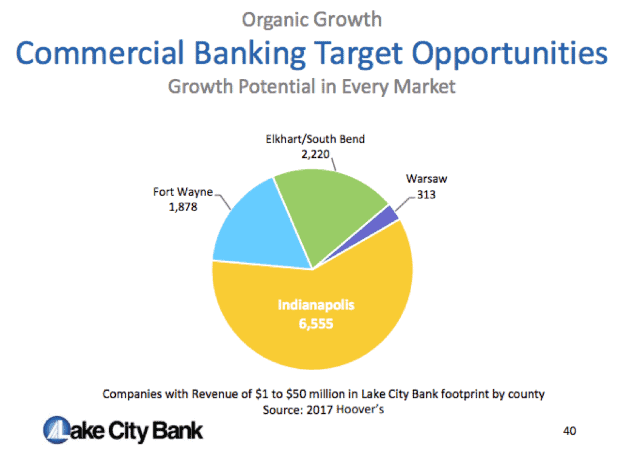

Indianapolis Expansion Provides Growth Potential

In addition to growing its non-interest income, LKFN’s primary driver of growth in the near future will be expanding into the Indianapolis market. LKFN only entered Indianapolis in 2011, and it recently opened its 6th branch in the city.

In terms of market opportunity, Indianapolis dwarfs LKFN’s other markets. Figure 6, from the company’s Q1 investor presentation, shows that Indianapolis has more companies with revenue of $1 million to $50 million (LKFN’s target market for its commercial accounts) than its other three major markets combined.

Figure 6: LKFN’s Growth Potential in Indianapolis

Sources: LKFN Investor Relations

Right now, LKFN has just a 2% market share for deposits in Indianapolis. It’s unlikely that the bank will achieve a dominant position in this market, but even getting to a 4% market share in the city – equal to FRME – offers a significant growth opportunity.

Cheap Valuation Provides Significant Upside

Despite its solid track record of performance and significant growth potential, LKFN is priced for minimal profit growth. At its current price of ~$48/share, LKFN has a price to economic book value (PEBV) ratio of just 1.1. This ratio means the market expects LKFN to grow after-tax profit (NOPAT) by no more than 10% for the remainder of its corporate life. This expectation seems overly pessimistic for a company that has grown NOPAT by 13% compounded annually over the past 20 years.

Our reverse discounted cash flow (DCF) model shows that even with modest profit growth, LKFN has significant potential upside.

If LKFN can grow NOPAT by just 6.5% compounded annually – half its historical rate – for the next decade, the stock is worth $65/share today, a 37% upside from the current stock price. See the math behind this dynamic DCF scenario.

How Traditional Research Misses this Stock

LKFN’s strong track record of growth and cheap valuation leads to an obvious question: how has the market not recognized the value in this stock? We see two key factors that have allowed LKFN to fly under the radar:

- Lack of Analyst Coverage: Just 5 Wall Street analyst firms cover LKFN, and most of the firms are on the smaller side, so they don’t generate many headlines. In addition, 4 out of the 5 firms rate LKFN a Hold. Wall Street doesn’t see much potential to win business from LKFN – a small bank that doesn’t do acquisitions and has a safe balance sheet – so the big sell-side firms don’t have an incentive to cover the stock as they do firms with more investment banking potential.

- High Price/Book: LKFN has a price to book (P/B) ratio of 2.3, which is significantly above the median company in the Financials sector, which has a P/B of 1.3. Even though P/B has many flaws and has significantly underperformed over the past decade, many investors – and indexes – still heavily rely on it to measure value. LKFN’s strategy of avoiding acquisitions means that its balance sheet isn’t inflated by goodwill, which causes the company to look worse than its peers based on P/B.

Continued Growth Could Send Shares Higher

Due to the factors above, LKFN’s stock has been flat over the past two years even as its profits have grown significantly. It’s hard to predict what will break the stock out of this holding pattern, but we believe that if the company’s growth continues, the market will eventually take notice.

In particular, continued growth and expansion of new bank branches will increase LKFN’s book value, which will put it back on the radar of traditional value investors. LKFN has grown accounting book value by 10% compounded annually over the past five years, so its book value should catch up with its profitability soon.

In addition, LKFN – which currently has $4.9 billion in total assets – will likely top $5 billion in assets soon. $5 billion is regarded as a major milestone for banks, so hitting this threshold could lead to more analyst coverage and investor awareness.

Sustainable Competitive Advantage That Will Drive Shareholder Value Creation

Here’s a summary why we think the moat around Lakeland Financial’s business will enable the company to generate higher profits than the current valuation of the stock implies. This list of competitive advantages helps LKFN offer better products/services at a lower price and prevents competition from taking market share.

- Superior cost efficiency that allows the bank to earn higher margins than its peers

- Strong emphasis on training and corporate culture that leads to higher employee productivity

- Connection to its community that big banks can’t replicate

Corporate Governance Is Good, But Could be Improved

LKFN ties its executive compensation to a wide variety of performance metrics, including return on equity, return on average assets, revenue growth, diluted EPS growth, capital adequacy, efficiency ratio, and asset quality.

We believe that most of these targets are good, and some of the metrics that we usually don’t like – such as return on equity and EPS growth – aren’t as big a concern for a company that has little leverage and doesn’t engage in earnings manipulation.

Still, we’d prefer LKFN add return on invested capital as a performance metric. ROIC is the primary driver of valuation, so executives should be incentivized to maximize ROIC.

Dividends and Share Repurchase Offer 2.5% Yield

LKFN has increased its dividend in 8 consecutive years. The current quarterly dividend of $0.30/share provides an annualized 2.5% yield. LKFN’s investments in technology and expansion into Indianapolis means the company’s free cash flow yield has been below its dividend yield in recent years, but the company’s solid balance sheet means there’s little reason to worry about the sustainability of the dividend.

In addition to dividends, LKFN returns capital to shareholders through share repurchases. Historically, LKFN’s buyback activity has been limited. The company repurchased just $463 thousand (less than 1% of market cap) in shares last year. However, LKFN’s board authorized a $30 million (2.4% of market cap) buyback program in January, which creates potential for higher levels of buyback activity going forward.

Insider Trading and Short Activity are Minimal

Insider activity has been minimal over the past 12 months, with 55 thousand shares purchased and 58 thousand shares sold for a net effect of ~4 thousand shares sold. These sales represent less than 1% of shares outstanding.

There are currently 1.5 million shares sold short, which equates to 6% of shares outstanding and 23 days to cover. The thin volume of trading in the stock means that if shorts have to cover their bets, it could lead to a big spike in the stock price.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

As investors focus more on fundamental research, research automation technology is needed to analyze all the critical financial details in financial filings. Below are specifics on the adjustments we make based on Robo-Analyst[1] findings in Lakeland Financial’s fiscal 2018 10-K:

Income Statement: we made $11 million of adjustments, with a net effect of removing $5 million in non-operating income (2% of revenue). We removed $8 million in non-operating income and $3 million in non-operating expenses. You can see all the adjustments made to LKFN’s income statement here.

Balance Sheet: we made $107 million of adjustments to calculate invested capital with a net increase of $19 million. The most notable adjustment was $48 million in loan-loss reserves. This adjustment represented 9% of reported net assets. You can see all the adjustments made to LKFN’s balance sheet here.

Valuation: we made $8 million of adjustments with a net effect of decreasing shareholder value by $8 million. You can see all the adjustments made to LKFN’s valuation here.

Attractive Fund That Holds LKFN

The following fund receives our Attractive-or-better rating and allocates significantly to Lakeland Financial.

- Capitol Series Trust: Fuller & Thaler Behavioral Small-Cap Equity Fund (FTHFX) – 1.7% allocation and Attractive rating.

This article originally published on May 8, 2019.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Harvard Business School features the powerful impact of our research automation technology in the case New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.

1 Response to "Finding Growth and Value in the Financials Sector"

This is an amazing review—

At age 76, I have a short investment horizon, but this kind of analysis would have helped me build a different portfolio in my younger days.

I will pass this on to several younger associates.

Thanks,

Coleman Robinson