Question: Why are there so many mutual funds?

Answer: Mutual fund providers tend to make lots of money on each fund so they create more products to sell.

The large number of mutual funds has little to do with serving investors’ best interests. Below are three red flags investors can use to avoid the worst mutual funds:

1. Inadequate Liquidity

This issue is the easiest issue to avoid, and our advice is simple. Avoid all mutual funds with less than $100 million in assets. Low levels of liquidity can lead to a discrepancy between the price of the mutual fund and the underlying value of the securities it holds. Plus, low asset levels tend to mean lower volume in the mutual fund and larger bid-ask spreads.

2. High Fees

Mutual funds should be cheap, but not all of them are. The first step here is to know what is cheap and expensive.

To ensure you are paying at or below average fees, invest only in mutual funds with total annual costs below 1.72%, which is the average total annual cost of the 6433 U.S. equity Style mutual funds we cover. The weighted average is lower at 1.04%, which highlights how investors tend to put their money in mutual funds with low fees.

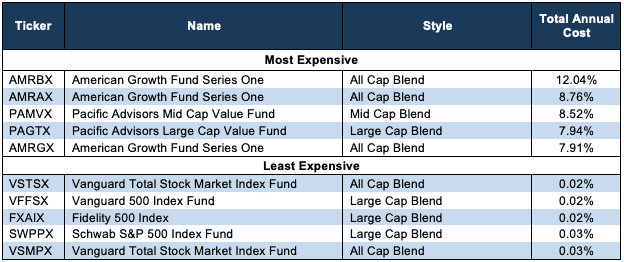

Figure 1 shows American Growth Fund Series One (AMRBX) is the most expensive style mutual fund and Vanguard Total Stock Market Index Fund (VSTSX) is the least expensive. American Growth Fund provides three of the most expensive mutual funds while Vanguard mutual funds are among the cheapest.

Figure 1: 5 Most and Least Expensive Style Mutual Funds

Sources: New Constructs, LLC and company filings

Investors need not pay high fees for quality holdings.[1] Vanguard Total Stock Market Index Fund (VSTSX) is the best ranked style mutual fund in Figure 1. VSTSX’s Neutral Portfolio Management rating and 0.03% total annual cost earns it an Attractive rating.[2] DWS CROCI U.S. Fund (DCURX) is the best ranked style mutual fund overall. DCURX’s Attractive Portfolio Management rating and 0.86% total annual cost earns it a Very Attractive rating.

On the other hand, Vanguard Extended Market Index Fund (VSEMX) holds poor stocks and earns our Unattractive rating, yet has low total annual costs of 0.07%. No matter how cheap a mutual fund, if it holds bad stocks, its performance will be bad. The quality of a mutual fund’s holdings matters more than its price.

3. Poor Holdings

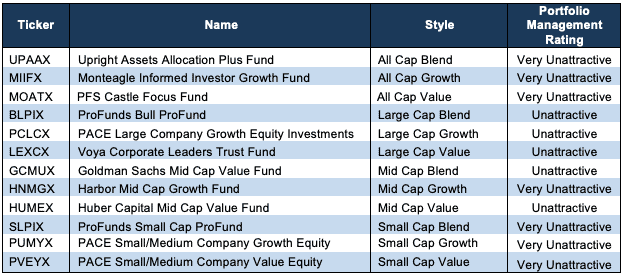

Avoiding poor holdings is by far the hardest part of avoiding bad mutual funds, but it is also the most important because a mutual fund’s performance is determined more by its holdings than its costs. Figure 2 shows the mutual funds within each style with the worst holdings or portfolio management ratings.

Figure 2: Style Mutual Funds with the Worst Holdings

Sources: New Constructs, LLC and company filings

PACE Select Advisors appears more often than any other providers in Figure 2, which means that they offer the most mutual funds with the worst holdings.

Upright Assets Allocation Plus Fund (UPAAX) is the worst rated mutual fund in Figure 2. Voya Corporate Leaders Trust Fund (LEXCX), PFS Castle Focus Fund (MOATX), Monteagle Informed Investor Growth Fund (MIIFX), PACE Small/Medium Company Growth Equity (PUMYX), Harbor Mid Cap Growth Fund (HNMGX), ProFunds Small Cap ProFund (SLPIX), PACE Large Company Growth Equity (PCLCX) and PACE Small/Medium Company Value Equity (PVEYX) also earn a Very Unattractive predictive overall rating, which means not only do they hold poor stocks, they charge high total annual costs.

Our overall ratings on mutual funds are on our stock ratings of their holdings and the total annual costs of investing in the fund.

The Danger Within

Buying a mutual fund without analyzing its holdings is like buying a stock without analyzing its business and finances. Put another way, research on mutual fund holdings is necessary due diligence because a mutual fund’s performance is only as good as its holdings’ performance. Don’t just take our word for it, see what Barron’s says on this matter.

PERFORMANCE OF MUTUAL FUND’s HOLDINGs = PERFORMANCE OF MUTUAL FUND

Analyzing each holding within funds is no small task. Our Robo-Analyst technology enables us to perform this diligence with scale and provide the research needed to fulfill the fiduciary duty of care. More of the biggest names in the financial industry (see At BlackRock, Machines Are Rising Over Managers to Pick Stocks) are now embracing technology to leverage machines in the investment research process. Technology may be the only solution to the dual mandate for research: cut costs and fulfill the fiduciary duty of care. Investors, clients, advisors and analysts deserve the latest in technology to get the diligence required to make prudent investment decisions.

This article originally published on July 25, 2019.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] This paper compares our analytics on a mega cap company to other major providers. The Appendix details exactly how we stack up.

[2] Harvard Business School features the powerful impact of our research automation technology in the case New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.