We published an update on this Long Idea on May 4, 2022. A copy of the associated Earnings Update report is here.

We published an update on this Long Idea on April 21, 2021. A copy of the associated Earnings Update report is here.

This best-in-class bank has the balance sheet to survive the COVID-driven economic crisis and is positioned to expand its market share as the economy recovers. JPMorgan Chase & Company (JPM: $91/share) is this week’s Long Idea.

Another Quality Business Trading at a Historical Discount

Over the past several weeks, we’ve identified high-quality businesses in some of the industries most adversely impacted by the COVID-19 pandemic. While evaluating restaurants, malls, homebuilders, airlines, insurers, hotels, and even advertising agencies, we have found several hidden gems including SYSCO Corporation (SYY), Darden Restaurants (DRI), Cracker Barrel Old Country Store (CBRL), Simon Property Group (SPG), D.R. Horton (DHI), Southwest Airlines (LUV), and Omnicom Group (OMC), Hyatt Hotels (H), and Allstate (ALL).

JPMorgan, with its industry-leading profitability, strong balance sheet, and undervalued stock presents another excellent buying opportunity for investors willing to look beyond the current economic crisis.

JPMorgan’s History of Profit Growth

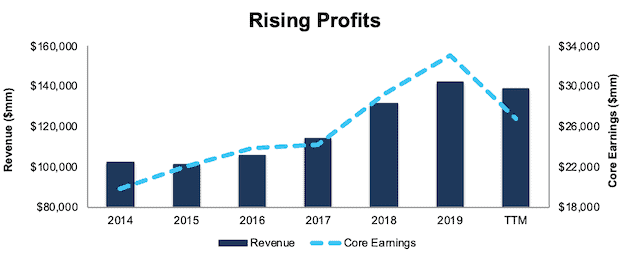

JPMorgan has a strong history of growing profits. Over the past five years, JPMorgan has grown revenue by 7% compounded annually and core earnings[1] by 11% compounded annually, per Figure 1. Since 2009, JPMorgan has grown core earnings by 10% compounded annually. The firm increased its core earnings margin year-over-year (YoY) in eight of the past ten years and from less than 11% in 2009 to 23% TTM. The drop in profits over the TTM period is what we call “the dip” and is evidence of COVID-19’s impact on the overall economy. However, whether the recovery is L shaped, U shaped, or V shaped, we expect JPMorgan’s profits to rebound over the long term.

Figure 1: JPMorgan’s Profitability Growth Since 2014

Sources: New Constructs, LLC and company filings.

JPMorgan’s improving profitability helps the business generate significant free cash flow (FCF). The company generated positive FCF in each of the past ten years and a cumulative $109 billion (39% of market cap) over the past five years. JPMorgan’s $31 billion in FCF over the TTM period equates to a 10% FCF yield, which is significantly higher than the Financials Sector average of 4%.

JPMorgan’s Balance Sheet is a Source of Strength

Unlike the 2008 Financial Crisis, in which many banks were under capitalized relative to their risky assets, banks’ balance sheets are much stronger going into the COVID-19 pandemic, JPMorgan included.

The results of the Federal Reserve’s Comprehensive Capital Analysis and Review (CCAR) showed that JPMorgan’s common equity Tier 1 (CET1) ratio would hold at a “very strong” 10%, and the firm would have in excess of $500 billion of liquid assets. The Federal Reserve’s stress test, which assumes unemployment peaking at 10% and the stock market falling 50%, results in JPMorgan’s revenue falling 20% and credit costs rising $20 billion over 2019. Even in such a pessimistic scenario, JPMorgan’s CET1 ratio would remain well above the regulatory requirements.

In addition to the Federal Reserve’s stress test, JPMorgan recently conducted its own test assuming an “extremely adverse scenario.” This scenario assumes an even deeper contraction of GDP from 2Q20 through 4Q20, down as much as 35%, with U.S. unemployment peaking at 14% in 4Q20. Under this scenario, the company would end the year with “strong liquidity” and a CET1 ratio of 9.5%, well above the regulatory requirements.

In addition to performing well in stress tests, JPMorgan’s financial strength is displayed through its loss absorbing capital – a measure of a firm’s capacity to absorb credit losses. According to this Wells Fargo analysis, JPMorgan’s loss absorbing capital, which accounts for capital above CET1 requirements, current reserves for credit losses, new earnings over three years, and additional capital required to fulfill future capital requirements, was enough to absorb net charge offs of 15.5% as of 1Q20. For comparison, at the peak of the Financial Crisis, the firm experienced only 8.6% net charge offs, or 6.9% below its current coverage.

Superior Profitability Matters in Down Times and When the Economy Recovers

COVID-driven disruptions may create liquidity issues for some less well-capitalized or financially sound banks. As a survivor, JPMorgan’s superior profitability and liquidity positions it to take the market share lost by weaker operators, generate goodwill with clients in times of need (such as providing loan relief/deferments), and return to its pre-crisis profit growth when the economy recovers.

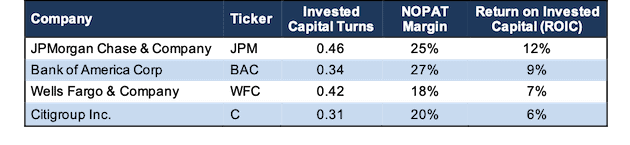

JPMorgan’s invested capital turns, a measure of balance sheet efficiency, rank highest among the four largest (by revenue) banks, which include JPMorgan, Bank of America Corp (BAC), Wells Fargo & Company (WFC), and Citigroup Inc. (C). JPMorgan’s net operating profit after-tax (NOPAT) margin of 25% ranks second highest among this group as well.

High margins and rising invested capital turns drive JPMorgan’s leading return on invested capital (ROIC). Per Figure 2, JPMorgan’s current ROIC of 12% is greater than its banking peers and well above the 7% earned at the depths of the Financial Crisis in 2008.

Figure 2: Superior Profitability vs. Competitors

Sources: New Constructs, LLC and company filings.

Unless you believe that there will be no demand for loans, bank deposits, asset management, investment banking, and many other banking products in the post-COVID world, it’s hard to argue against JPMorgan’s ability to survive. And, if it survives, it’s had to argue that the firm’s best-in-class profitability before the crisis will not translate into more market share and profit growth after the crisis.

Well-Positioned for Continued Growth – Even in Low Interest Environment

We’ve long argued that low interest rates are the new normal. However, that hasn’t stopped the notion of “lower for longer” interest rates worrying many investors about the future profitability of the bank industry as a whole.

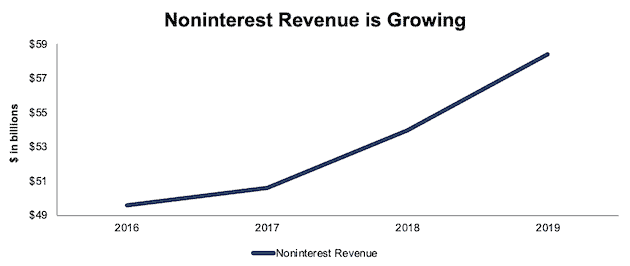

However, worrying only about interest rates ignores the other half of JPMorgan’s business. Since 2016, JPMorgan’s noninterest revenue, which includes investment banking fees, deposit-related fees, asset management, components of card income, and more has grown from $50 billion to $58 billion in 2019. Over the TTM period, noninterest revenue consisted of half of the firm’s total net revenue, which is defined as noninterest revenue plus interest income minus interest expense.

Figure 3: JPMorgan’s Noninterest Revenue Since 2016

Sources: New Constructs, LLC and company filings.

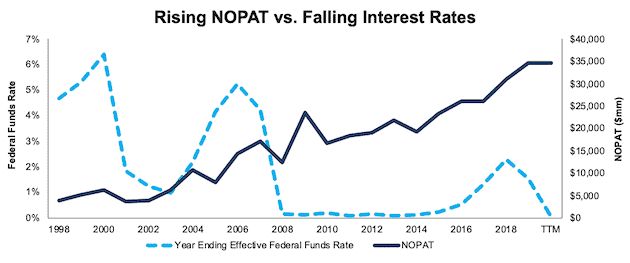

Additionally, lower interest rates don’t necessarily mean declining profits. At the end of 2007, the Federal Funds Rate was 4.2%. By the end of 2008, the Federal Funds Rate had fallen to 0.16%. This lower-rate environment persisted all the way through 2014 when the Federal Funds Rate was 0.12%. However, JPMorgan actually grew net operating profit after-tax (NOPAT) 2% compounded annually over this seven-year period. Per Figure 4, the Federal Funds Rate has fallen from 4.68% in 1998 to 0.05% today while JPMorgan’s NOPAT increased from $3.8 billion in 1998 to $34.7 billion over the TTM. Even if a lower rate environment persists, we would expect JPMorgan to continue its ability to grow profits over the long term.

Figure 4: JPMorgan’s NOPAT vs Effective Federal Funds Rate Since 1998

Sources: New Constructs, LLC and Federal Reserve Economic Data

Low or even negative-interest-rate policies often hurt smaller banks focused on domestic loans and deposits more than larger banks, which tend to be more diversified across currencies and have larger fee-based businesses. JPMorgan’s size and diversification provide ample opportunity to attract more assets and more market share as smaller banks are forced to exit a low-interest rate environment.

It’s Not 2008 Again

While the market is pricing the banking industry as if the 2008 Financial Crisis will recur, it is important to note significant differences between then and now.

In 2008, the risky lending practices employed by the banking industry caused the Financial Crisis and subsequent Great Recession. The U.S. banking system is much stronger this time around.

We previously mentioned JPMorgan’s financial strength, however, several of the largest U.S. banks are also in a stronger position now than they were before the 2008 Financial Crisis. In 2008, JPMorgan, Citigroup, Bank of America, U.S. Bancorp (USB), and PNC Financial Services Group, Inc. (PNC) as a group, had enough loss absorbing capital to cover loan losses of just 8%. Today, these banks collectively have enough capital to absorb losses on 13% of their loans.

In the current crisis, instead of being part of the problem, banks are playing a key role in delivering solutions. JPMorgan’s financial strength has enabled it to support the economy at its present point of need. In its 1Q20 earnings call, the firm noted it participated in the Paycheck Protection Program with over 300,000 applications representing $37 billion worth of loans, extended more than $100 billion in new credit in March, and helped clients raise $380 billion of investment grade debt during the first quarter.

The Economy is Expected to Rebound

The International Monetary Fund (IMF) and nearly every economist in the world believe the global economy will grow strongly in 2021. The IMF estimates the global economy will expand by 5.8%, and the U.S. economy by 4.7%, in 2021. The overall growth in the economy should lead to a rebound in the banking industry as business activity and consumer spending grow once again.

Among those expecting an economic recovery is Federal Reserve Chairman Powell who noted in a recent interview that he expects the economy to grow in the second half of 2020.

Part of Chairman Powell’s confidence in a recovery most certainly comes from the speed and magnitude of actions taken by Congress, the U.S. Department of the Treasury, and the Federal Reserve in reducing the financial stress caused by the pandemic. While the steps taken so far are substantial, the Fed chairman knows there’s plenty more ammunition to drive economic growth if needed.

In his latest annual letter to shareholders, JPMorgan’s Chairman & CEO Jamie Dimon highlighted additional action the Treasury and Federal Reserve could take should the need arise including balance sheet expansion, additional lending facilities, and changes to the banking industry’s capital and liquidity requirements that could work to strengthen the U.S. economy and support a recovery.

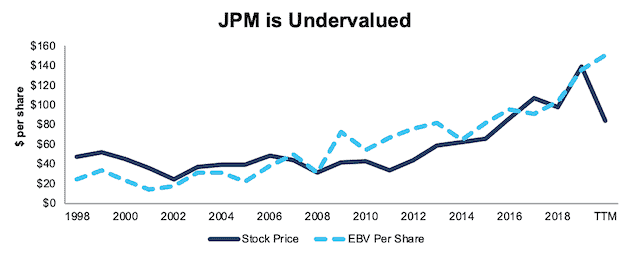

JPM Trades at a Discount

Despite entering the current crisis from a position of strength, JPM is down 33% YTD and now trades at its cheapest price-to-economic book value (PEBV) ratio (0.6) since 2012, and nearly equal to 2009. This ratio means the market expects JPMorgan’s NOPAT to permanently decline by 40%. This expectation seems overly pessimistic over the long term.

JPMorgan’s current economic book value, or no-growth value, is $150/share – a 65% upside to the current price.

Figure 5: Stock Price vs. Economic Book Value (EBV)

Sources: New Constructs, LLC and company filings.

Current Price Implies Another Global Financial Crisis Is Coming

Below, we use our reverse DCF model to quantify the cash flow expectations baked into JPMorgan’s current stock price. Then, we analyze the implied value of the stock based on different assumptions about COVID-19’s impact on the economy and JPMorgan’s future growth in cash flows.

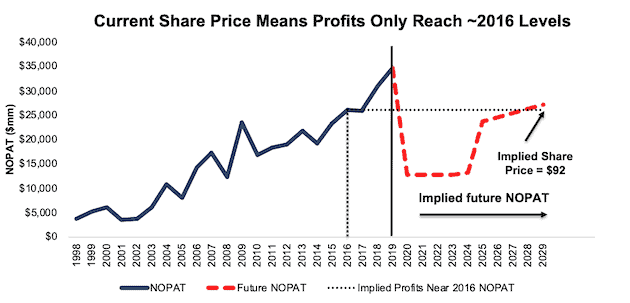

Scenario 1: Using recent projections for revenue declines, historical margins, and average historical GDP growth rates, we can model the worst-case scenario already implied by JPMorgan’s current stock price. In this scenario, we assume:

- NOPAT margins fall to 12% (equal to 2008 and lowest in the history of our model vs. 25% TTM) from 2020-2023 before rebounding to 21% (company average since 2009) in 2024 and each year thereafter

- Revenue falls 26% in 2020 (vs. consensus -5.54% and double the year-over-year decline in 2008) and does not grow from 2021 to 2024 (vs. consensus 1.86% in 2021 and 1.89% in 2022)

- Revenue grows 3.5% in 2025 and each year thereafter, which equals the average global GDP growth rate since 1961

In this scenario, where JPMorgan’s NOPAT declines 2% compounded annually over the next decade (and 18% compounded annually from 2019-2024), the stock is worth $92/share today – nearly equal to the current stock price. See the math behind this reverse DCF scenario.

Figure 6 compares the stock’s implied future NOPAT to the firm’s historical NOPAT for this scenario. This worst-case scenario implies JPMorgan’s NOPAT 10 years from now will be 21% below its 2019 NOPAT. In other words, this scenario implies that 10 years after the COVID-19 pandemic, JPMorgan’s profits will have only recovered to ~2016 levels. In any scenario better than this one, JPM holds significant upside potential, as we’ll show in below in scenario 2.

Figure 6: Current Valuation Implies Severe, Long-Term Decline in Profits: Scenario 1

Sources: New Constructs, LLC and company filings.

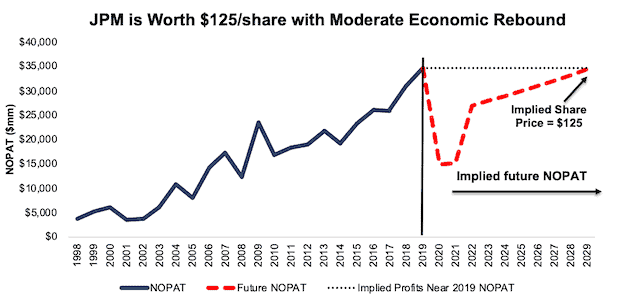

Scenario 2: Long-Term View Could Be Very Profitable

If we assume, as does the IMF and nearly every economist in the world, that the global economy rebounds and returns to growth starting in 2021, JPM is highly undervalued.

In this scenario, we assume:

- NOPAT margins fall to 12% (equal to 2008 and lowest in the history of our model vs. 25% TTM) from 2020-2021 before rebounding to 21% (ten-year average) in 2022 and each year thereafter

- Revenue falls 13% in 2020 (same year-over-year decline as 2008) and grows in line with consensus estimates at 1.86% in 2021 and 1.89% in 2022

- Revenue grows 3.5% in 2023 and each year thereafter, which equals the average global GDP growth rate since 1961

In this scenario, JPMorgan’s NOPAT declines less than 1% compounded annually over the next decade (and 57% YoY in 2020), and the stock is worth $125/share today – a 37% upside to the current price. See the math behind this reverse DCF scenario.

For comparison, JPMorgan has grown NOPAT by 13% compounded annually over the past five years and 10% compounded annually over the past two decades. It’s not often investors get the opportunity to buy an industry leader at such a discounted price.

Figure 7 compares the stock’s implied future NOPAT to the firm’s historical NOPAT in scenario 2. This scenario implies that ten years from now, the firm’s NOPAT will be 1% lower than its 2019 level. For context, JPMorgan exceeded its pre-Financial Crisis NOPAT level in just two years: the firm grew NOPAT from $17.2 billion in 2007 to $23.4 billion in 2009. If the firm’s profits return to the 2019 level in less than 10 years, JPM has even more upside potential.

Figure 7: Implied Profits Assuming Global Recovery Starts in 2021: Scenario 2

Sources: New Constructs, LLC and company filings.

Sustainable Competitive Advantages Will Drive Shareholder Value Creation

Here’s a summary of why we think the moat around JPMorgan’s business will enable it to continue to generate higher NOPAT than the current market valuation implies. The following competitive advantages help JPMorgan survive the downturn and return to growth as the economy grows again:

- Strong balance sheet to survive the dip

- Half of JPMorgan’s net revenue comes from noninterest revenue sources

- Superior profitability to its main competitors

What Noise Traders Miss with JPMorgan

These days, fewer investors focus on finding quality capital allocators with shareholder friendly corporate governance. Instead, due to the proliferation of noise traders, the focus is on short-term technical trading trends while high-quality fundamental research is overlooked. Here’s a quick summary of what noise traders are missing:

- Consistent profit growth over the past two decades in the face of declining interest rates

- Banks are part of the solution to the current economic downturn

- Valuation implies the banking industry faces a crisis worse than 2008

Nearly 4% Yield with Potential for More

JPMorgan has paid dividends in each of the past 10 years. Over the past five years, the firm has generated more in free cash flow ($109 billion) than it has paid out in dividends ($98 billion), which equates to an average $2.2 billion surplus each year. It’s latest quarterly dividend, when annualized, equals $3.60/share or a 3.9% dividend yield.

Firms with cash flows greater than dividend payments have a higher likelihood to maintain and grow dividends. While JPMorgan has a very strong balance sheet, the firm may choose to suspend its dividend “out of extreme prudence” if the current crisis deepens. Even so, investors buying at current prices could get a nice yield with upside potential if JPMorgan reinstated the dividend over the long term.

In addition to dividends, JPMorgan historically returned capital to shareholders through share repurchases. On March 15, 2020, JPMorgan temporarily suspended its share repurchases through the second quarter of 2020 in response to the COVID-19 pandemic.

JPMorgan has repurchased $10.8 billion worth of shares since 2015 (27% of current market cap). Prior to the suspension, JPMorgan had an additional $9.2 billion remaining under its current authorization, which expires on June 30, 2020. Should the firm resume share repurchases, the yield for investors will increase.

A Consensus Beat or Signs of Recovery Could Send Shares Higher

According to Zacks, consensus estimates at the end of February pegged JPMorgan’s 2020 EPS at $10.75/share. Jump forward to May 19, and consensus estimates for JPMorgan’s 2020 EPS have fallen to $5.13/share.

Though the COVID shutdowns are crushing near-term profits, these lowered expectations provide a great opportunity for a strong business, such as JPMorgan, to beat consensus, if not this quarter, then maybe the next. Though our current Earnings Distortion Score for JPMorgan is “In-Line”, the firm beat EPS estimates in 10 of the past 12 quarters, and doing so again, in the midst of such market turmoil, could send shares higher.

Additionally, any signs of a recovery in the U.S. economy would send shares higher.

Executive Compensation Plan Could Be Improved

No matter the macro environment, investors should look for companies with executive compensation plans that directly align executives’ interests with shareholders’ interests. Quality corporate governance holds executives accountable to shareholders by incentivizing them to allocate capital prudently.

In fiscal 2019, 83% of the CEO’s variable pay and 30% of the firm’s other named executive officers’ (NEO’s) variable pay were linked to objective targets based on absolute and relative return on tangible common equity (ROTCE).

While we applaud JPMorgan for significantly linking executive compensation to a measure of profitability, we would still prefer the firm use an accurate ROIC calculation, as there is a strong correlation between improving ROIC and increasing shareholder value. Having accurate values for NOPAT and invested capital closes accounting loopholes and ensures management is accountable for every dollar invested into the company over the entirety of its life.

Despite using flawed metrics for measuring performance, JPMorgan’s plan has not compensated executives while destroying shareholder value. JPMorgan has grown economic earnings by 86% compounded annually over the past five years and 6% compounded annually over the past decade.

Insider Trading and Short Interest Trends

Over the past twelve months, insiders have bought a total of 371 thousand shares and sold 2.3 million shares for a net effect of 1.9 million shares sold. These sales represent less than 1% of shares outstanding.

There are currently 24.1 million shares sold short, which equates to 1% of shares outstanding and 1 day to cover. Short interest is down 17% from the prior month. The lack of short interest indicates that the market is not willing to bet against this stock’s chances to rebound.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

As investors focus more on fundamental research, research automation technology is needed to analyze all the critical financial details in financial filings as shown in the Harvard Business School and MIT Sloan paper, "Core Earnings: New Data and Evidence”.

Below are specifics on the adjustments we make based on Robo-Analyst findings in JPMorgan Chase & Company’s 2019 10-K:

Income Statement: we made $6.0 billion of adjustments, with a net effect of removing $2 million in non-operating expenses (<1% of revenue). You can see all the adjustments made to JPMorgan Chase’s income statement here.

Balance Sheet: we made $58.2 billion of adjustments to calculate invested capital with a net increase of $37.2 billion. One of the largest adjustments was $16.1 billion in goodwill. This adjustment represented 6% of reported net assets. You can see all the adjustments made to JPMorgan Chase’s balance sheet here.

Valuation: we made $51.4 billion of adjustments with a net effect of decreasing shareholder value by $40.1 billion. The most notable adjustment to shareholder value was $30.1 billion in preferred stock. This adjustment represents 11% of JPM’s market cap. See all adjustments to JPMorgan Chase’s valuation here.

Attractive Funds That Hold JPM

The following funds receive our Attractive rating and allocate 5% or more to JPMorgan Chase & Company:

- ProFunds Banks UltraSector Fund (BKPIX) – 20% allocation

- iShares U.S. Financial Services ETF (IYG) – 12% allocation

- State Street Select Financial Select Sector SPDR Fund (XLF) – 12% allocation

- First Trust Nasdaq Bank ETF (FTXO) – 9% allocation

- Invesco KBW Bank ETF (KBWB) – 9% allocation

- BlackRock Exchange Portfolio (STSEX) – 7% allocation

- Holland Balanced Fund (HOLBX) – 7% allocation

- Bretton Fund (BRTNX) – 5% allocation

- Haverford Quality Growth Stock Fund (HAVGX) – 5% allocation

- FMI Large Cap Fund (FMIQX) – 5% allocation

- Amplify CWP Enhanced Dividend Income ETF (DIVO) – 5% allocation

- iShares Morningstar Large Cap Value ETF (JKF) – 5% allocation

- Brandywine Global (LBISX) – Diversified U.S. Large Cap Value Fund – 5% allocation

- Invesco Buyback Achievers ETF (PKW) – 5% allocation

- Matrix Advisors Value Fund, Inc (MAVFX) – 5% allocation

This article originally published on May 21, 2020.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Our core earnings are a superior measure of profits, as demonstrated in In Core Earnings: New Data & Evidence a paper by professors at Harvard Business School (HBS) & MIT Sloan. The paper empirically shows that our data is superior to “Income Before Special Items” from Compustat, owned by S&P Global (SPGI).

3 replies to "Bank on the Best"

Great Analysis

This is not a criticism, but why JPM ranked 40th over MS ranked 1 or BKU ranked 19th as your best long idea? I included BKU because its my idea for the current conditions. If you have time, let me know. I could be wrong on BKU, Eldon Brickle

Hi Eldon:

Thanks for your comment!

TO whose rankings are your referring?

Who ranks JPM 40th over MS #1?