This report is one of a series on the adjustments we make to GAAP data so we can measure shareholder value accurately. This report focuses on an adjustment we make to our calculation of economic book value and our discounted cash flow model.

We’ve already broken down the adjustments we make to NOPAT and invested capital. Many of the adjustments in this third and final section deal with how adjustments to those two metrics affect how we calculate the present value of future cash flows. Some adjustments represent senior claims to equity holders that reduce shareholder value while others are assets that we expect to be accretive to shareholder value.

Adjusting GAAP data to measure shareholder value should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

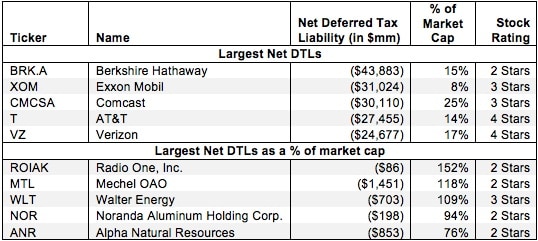

Deferred tax assets (DTAs) arise when reported income on a financial statement is less than taxable income, and deferred tax liabilities (DTLs) come about when reported income is greater than taxable income. DTAs are accounts set aside for the reduction of future taxes while DTLs are accounts for the payment of taxes in the future. Both of these items are a result of differences between GAAP accrual accounting and tax policy. We’ve already covered how DTAs and DTLs affect invested capital in a separate report. However, these accounts affect a company’s discounted cash flow model as well.

We subtract net deferred tax liabilities (DTLs minus DTAs) from our calculation of shareholder value as they are real future cash obligations that limit the amount of money available for distribution to shareholders.

4 replies to "Net Deferred Tax Assets and Liabilities – Valuation Adjustment"

Hello,

Absolutely love this website.

If we have a net DTA do we add that to Invested capital (the opposite of what was done with net DTLs here) ?

Thanks

Correction : “do we add that to EBV”? Not invested capital.

I’m glad you love the website, and thanks for your good question.

We do not add net DTA’s to EBV for two primary reasons:

1. DTA values on the balance sheet don’t accurately reflect the value attributable to shareholders, both because they rely on assumptions about future profitability, and because these are potential future savings that are not discounted to their present value.

2. Unlike with other assets that we add to EBV like excess cash or discontinued operations, DTA’s cannot be quickly translated into shareholder value. If a firm needs to raise money, they cannot sell DTA’s.

Ok understandable. I was reading more on deferred tax assets and came to the same conclusion as well but was unsure. I appreciate the quick response.

Thank you!!!!