We published an update on this Long Idea on October 4, 2023. A copy of the associated report is here.

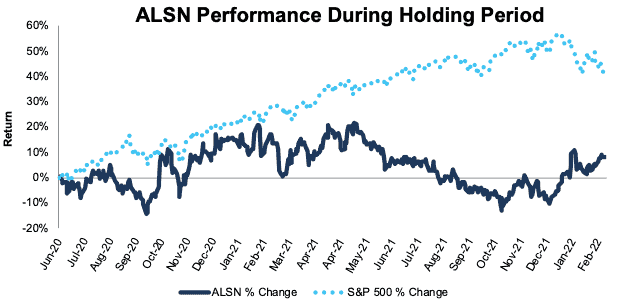

We made Allison Transmission Holdings (ALSN: $40/share) a Long Idea in June 2020, as part of our “See Through the Dip” thesis. Since then, the stock is up 6% compared to a 40% gain for the S&P 500. Though the company’s profits have recovered since the COVID-induced dip in production, the stock price is still below pre-pandemic levels and offers strong upside, to $134+/share. See our most recent report from March 2021 on Allison Transmission here.

We leverage more reliable fundamental data, as proven in The Journal of Financial Economics[1], and shown to provide a new source of alpha, with qualitative research to pick this Long Idea.

Allison Transmission’s Stock Could Triple Based on:

- Market share gains during the industry-wide downturn in production prove the strength of the business model.

- Continued labor shortages in the trucking industry, strong demand for transportation, and product innovation provide opportunities for additional market share gains.

- Fears that the company will become irrelevant are overblown as Allison Transmission is well-positioned to supply an industry shifting towards electrification.

- The current valuation of the stock implies profits will permanently fall 60% below current levels.

Figure 1: Long Idea Performance: From Date of Publication Through 2/22/2022

Sources: New Constructs, LLC

What’s Working

Performance Keeps on Trucking: After a “dip” in production during 2020, the company’s revenue and Core Earnings saw an upswing in 2021. Allison Transmission’s revenue in 4Q21 rose 20% year-over-year (YoY) and revenue for the entire year rose 15% over 2020. Best of all, the company’s revenue growth led to a 37% YoY improvement in Core Earnings.

Service Parts Segment Grows During Supply Chain Disruption: Industry-wide disruptions to truck manufacturers’ supply chains drives operators to service older trucks in their fleets rather than replacing them. With a large service parts business, Allison Transmission benefits from the increase in maintenance spending. The company’s service parts segment revenue as a percent of total grew from 20% in 2019 (before the pandemic) to 22% in 2021.

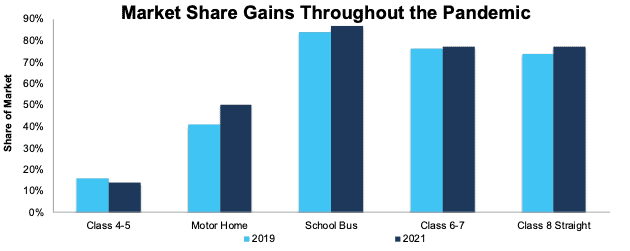

Industry Leader Takes Market Share: Though the truck manufacturing industry has faced labor and supply chain challenges since the pandemic, the strength of Allison Transmission’s operation positioned the company to grow its share in four of its five largest markets, per Figure 2.

Figure 2: Allison Transmission’s Market Share: 2019 Vs. 2021

Sources: New Constructs, LLC and 2019 & 2021 company 10-Ks

Product Innovation Drives Growth: Allison Transmission invests in innovations to help the company grow in its existing and new markets with products such as:

- 3414 Regional Haul Series, which plays a key role in growing its share of the Class 8 tractor market

- Allison 1000 series, which achieved 40% share of the Korean light-duty market within the first year of release

- Allison 4000 series, which is used in wide-body mining in China and has potential to add $50 million in incremental annual revenue

- Allison 3000 series, which will include the product line’s first 9-speed transmission

- eGen Flex series, which improves fuel economy by 25% versus conventional diesel busses

- eGen Power series, which are electric axles designed to replace powertrains of conventional trucks and busses

- FracTran, which is positioned to grow along the long-term demand for natural gas

EV Is a Growth Opportunity: Allison Transmission’s manufacturing experience, ability to innovate, experience with electric propulsion systems, and industry relationships, position the company to be a key supplier of hybrid and electric propulsion systems. Allison Transmission already designs and manufactures hybrid and fully electric propulsion systems, which are designed to extend range. The company is already delivering results with its electric axels used in hybrid busses and electric trucks.

What’s Not Working

Sales and Profits Are Still Below Pre-Pandemic Levels: Despite improvement in 2021 over 2020, Allison Transmission’s 2021 revenue was 11% below 2019. Core Earnings in 2021 were 15% below 2019 levels. However, the company expects to reach near pre-pandemic levels in 2022. The midpoint of management’s revenue guidance for 2022 is $2.7 billion, which is equal to 2019. The high-end of the guidance would be its largest annual revenue level ever.

Rising R&D Spending Is Likely to Continue: To meet the challenge of adapting to changing demand, Allison Transmission invests heavily in research and development (R&D). The company increased its R&D spend in 4Q21 25% YoY to $50 million. Even with increased the increased R&D spend, the company generates plenty of free cash flow (FCF). In 4Q21, Allison Transmission’s FCF of $147 million rose 27% YoY and reached its highest level since 1Q19.

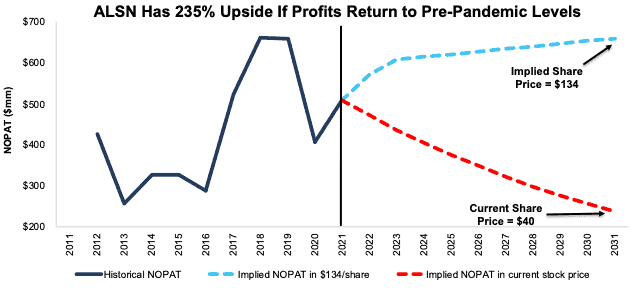

Allison Transmission Is Priced for Profits to Fall 60% Below TTM Levels

Allison Transmission’s price-to-economic book value (PEBV) ratio of 0.4 means the stock is priced for profits to fall, permanently, by 60% from current levels. Below, we use our reverse discounted cash flow (DCF) model to analyze the expectations for future growth in cash flows baked into a couple of stock price scenarios for Allison Transmission.

In the first scenario, we assume Allison Transmission’s:

- NOPAT margin remains at 21% (equal to 2021) from 2022 – 2031, and

- revenue falls 7% (vs. 2022 – 2023 consensus estimate CAGR of +9%) compounded annually from 2022 – 2031).

In this scenario, Allison Transmission’s NOPAT falls 7% compounded annually from 2022 – 2031, and the stock is worth $40/share today – equal to the current price. In this scenario, Allison Transmission’s NOPAT in 2031 is just $238 million, its lowest NOPAT since 2012 and less than half its 2021 NOPAT.

Allison Transmission Could Reach $134 or Higher

If we assume Allison Transmission’s:

- NOPAT margin remains at 21% (vs. five-year average of 23%) from 2022 – 2031,

- revenue falls 7% (equal to 2022 – 2023 consensus estimates) compounded annually from 2022 – 2023, and

- revenue grows by just 1% compounded annually from 2024 – 2030, then

the stock is worth $134/share today – 235% above the current price. In this scenario, Allison Transmission’s NOPAT in 2031 is $659 million, or nearly equal to its pre-pandemic NOPAT in 2019. Should Allison Transmission’s NOPAT rise above pre-pandemic levels, the stock has even more upside.

Figure 3: Allison Transmission’s Historical and Implied NOPAT: DCF Valuation Scenarios

Sources: New Constructs, LLC and company filings

This article originally published on February 23, 2022.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, sector, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Our research utilizes our Core Earnings, a more reliable measure of profits, as proven in Core Earnings: New Data & Evidence, written by professors at Harvard Business School (HBS) & MIT Sloan and published in The Journal of Financial Economics.